Does the eruption of the White Island volcano spell the end for ‘volcano tourism’?

Could the eruption of the White Island volcano on 9 December last year spell the end for ‘volcano tourism’? In the aftermath of the tragedy, cruise lines and travel insurers may be considering their position on cover for such activities. Robin Gauldie asked industry experts for their take on the issue

The unforeseen eruption on a tiny, privately owned volcanic island just off the coast of New Zealand killed 17 people, including tour guides and cruise passengers. At the time of writing, 13 people were still in hospital with severe burns, and two remained missing.

Regular visits

Volcano tours are popular shore excursions for cruise passengers. Most of the 47 people on White Island at the time of the eruption were passengers from the Royal Caribbean vessel Ovation of the Seas, several of whom were among the fatalities. Soon after the incident, Royal Caribbean announced that it had suspended all tours of active volcanoes.

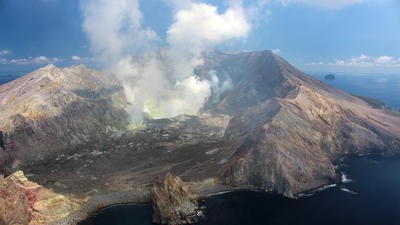

Small, slumbering volcanoes like White Island, as well as awesome giants from Hawaii to the Mediterranean, have become magnets for a wide range of visitors

Despite the highly publicised event, most ‘volcano tourism’ remains an acceptable risk, according to travel insurers. Deciding when visiting a volcano becomes a foreseeable hazard, though, is made trickier due to the lack of an internationally accepted system of eruption warnings. Nevertheless, small, slumbering volcanoes like White Island, as well as awesome giants from Hawaii to the Mediterranean, have become magnets for a wide range of visitors.

Package holidaymakers and cruise ship passengers swim happily in sea heated by undersea vents and wander among volcanic rocks at Nea Kameni, an islet off Santorini, one of Greece’s most popular holiday islands. Perhaps they’re unaware that Santorini’s spectacular, sea-filled caldera was created around 4,000 years ago by an apocalyptic event that destroyed Europe’s first civilisation, or that Nea Kameni last erupted as recently as 1950. Or perhaps that’s part of the thrill.

Also in Greece, day-trippers in search of an exotic setting for an Instagram selfie troop to tiny Nissiros, close to the popular resort island of Kos, to discover a dormant crater filled with bubbling, sulphurous mud pools. In Italy, Vesuvius and Stromboli – which has been in continuous eruption for almost 90 years – attract thousands of visitors.

Volcano Discovery, a specialist tour operator based in Germany, features ‘adventure guaranteed’ trips to volcano destinations such as Stromboli, Santorini, Krakatau in Indonesia and the remote Kurile Islands off Russia’s Pacific coast. Insurance provided by World Nomads is offered on the operator’s website.

Still insurable

Despite recent events, World Nomads spokesperson Phil Sylvester does not believe volcano tourism is likely to become an uninsurable hazard. “We discussed this in the immediate aftermath of the White Island tragedy,” he says. “We came to the conclusion that we have sufficient safeguards in place from a risk point of view, considering licensing of operators, warning and alert systems and, ultimately, the obligation on insureds to not take ‘unnecessary risk’.”

Sylvester draws comparisons with other activities that may appear hazardous, but are in reality low risk. “Consider bungee jumping, which was also popularised in New Zealand,” he says. “If you tied a bunch of elastic bands to your legs and jumped off the roof of your hotel, I can confidently predict no insurer would entertain a claim. But if an insured with appropriate cover turns up at a provider who has passed safety audits and consequently holds a license to operate, follows all their safety procedures, takes directions from their staff and doesn’t do anything stupid, it is highly unlikely that any harm will come to them, and if it does it would be ‘unforeseen’ and extraordinary.”

For those visitors to White Island, the criteria above seem to have been met. Sylvester said to ITIJ: “The operator was licensed, safety equipment was used, a trained guide accompanied all visitors [and] the eruption alert was below the level which would have precluded a visit.” He added: “Perhaps official inquiries will recommend that the criteria for future visits to volcanoes need to be tightened, which would seem prudent as any loss of life is truly terrible. If the threshold for volcano tours was lowered, our current test for extending cover would remain effective,” Sylvester confirmed.

The reputation of travel insurers could be damaged, he added, if the industry were to take a more draconian approach to such cover: “The public already eyes the product disclosure statement (PDS) and policy wording with suspicion. While adding clauses may help insurers manage risk, it is very likely to add to ambiguity and confusion for the end user. It is important for insurers to strike a balance between managing risk and providing a great customer experience.”

Kasara Barto, Public Relations Manager at US-based travel insurance comparison website Squaremouth, agreed that a measured approach is appropriate: “It would be unlikely that insurers would exclude coverage for dormant volcanoes outright,” she said. “However, once an event occurs, or becomes known or expected, providers will no longer offer coverage for that event on any policies purchased after that date. [So] while insurers probably won’t exclude dormant volcanoes specifically, they can stop providing coverage for losses related to a volcanic eruption once it becomes ‘foreseen’.”

The general exclusion in travel insurance policies around the world for foreseen events, noted Barto, can be applied to a volcanic eruption. “An example of this wording is: ‘any issue or event that was not anticipated or expected and occurs after the effective date of coverage’.”

Risk assessment

Managing and assessing risk is tricky when it comes to volcanoes, though. Predicting eruptions is not an exact science, even in comparison with monitoring events such as hurricanes, blizzards and avalanches.

Writing in online publication The Conversation in the aftermath of the White Island eruption, Shane Cronin, Professor of Earth Sciences at the University of Auckland, New Zealand, pointed out that such explosive hydrothermal (steam-driven) eruptions can happen without warning and are much harder to track using existing monitoring systems than a magma eruption, such as those seen in volcanoes such as Vesuvius, Stromboli or Hawaii’s Mt Pele (all of which are also popular volcano tourism destinations). Once a hydrothermal event is underway, those nearby have only minutes or even seconds to react, Professor Cronin stated.

Vulcanologists also point out that each volcano is unique, so monitoring all the world’s potential volcano tourism sites seems an impossible dream. Nor is there a standardised worldwide system of alert levels.

New Zealand’s GeoNet monitoring service operates a five-rung volcanic alert system system, from level zero – indicating no volcanic unrest – to level five, indicating a major eruption. GeoNet’s volcanic alert bulletin of 3 December (six days before the White Island eruption) placed White Island at level two: ‘moderate volcanic unrest’.

Should the industry create a risk assessment process down to specific volcanoes? No.

White Island is not the only volcanic incident to cause tourist deaths in recent years. In September 2014, 63 hikers were killed when Mount Ontake in Japan erupted.

Japan, a densely populated island nation with more than 100 active volcanoes, has the world’s most sophisticated – and plain-spoken – volcano monitoring system. On the Japan Meteorological Agency’s five-level scale, level one indicates potential for increased activity. At level two, a ‘near crater warning’ kicks in, instructing ‘do not approach the crater’. Presumably, therefore, insurers would regard any advisory above level one as indicating a ‘foreseen risk’.

The US Geological Survey’s (USGS) alert system, by contrast, is fuzzier. Level zero or ‘normal’ indicates a ‘non-eruptive state’; level two or ‘advisory’ indicates ‘elevated unrest’; level three or ‘watch’ indicates ‘increased potential of eruption’; and level four or ‘warning’ indicates ‘hazardous eruption imminent, under way or suspected’. Insurers erring on the side of caution might look at the USGS’s level two as uninsurable. Even those with a higher appetite for risk would probably balk at level three.

Disparate as they are, various national vulcanism monitoring and warning systems have one thing in common: their priority is preventing mass casualties by providing timely evacuation warnings to residents of cities in the shadow of active volcanoes, such as Popocatépetl, 40 miles from Mexico City, or Taal, a similar distance from Manila, capital of the Philippines. Both erupted powerfully in January 2020, with thousands of residents forced to flee.

But, compared with safeguarding the lives of tens of thousands of people living near major volcanoes, monitoring small and remote locations that are visited by comparatively tiny numbers of tourists is a relatively low priority for national warning systems.

“Volcanoes have always been dangerous and there are different levels of risk, but travel companies are exploring their destinations as the demand for new experiences grows,” says Greg Lawson, Head of Travel Insurance for UK-based Collinson Group. “Where demand grows, niche travel and insurance industries will adapt as they did for climbing Mt Everest, for example. Should the travel industry ensure it can deliver such activities safely and transparently? Yes, it should. Should the travel insurance industry keep an eye and review claims impacts? Yes. Should the industry create a risk assessment process down to specific volcanoes? No.”

Culture of recklessness?

Media coverage of the White Island eruption also homed in on New Zealand’s government-run accident compensation scheme, which pays for medical treatment for New Zealanders and visitors injured in accidents of any kind. The scheme effectively blocks the accident victim from launching a negligence suit against other parties, including tour operators. Some sources credit the scheme with fostering New Zealand’s transformation into a world leader in ‘adventure experience’ tourism – and arguably fostering a culture of recklessness among adventure tourists. Insurers rebut that claim, though.

Activities that verge on the reckless remain a niche pursuit, says Sylvester of World Nomads. “We continue to cover more than 130 adventure activities, but some of the most daring, like wing-suit flying, remain outside the ambit of our cover,” he told ITIJ. “There has been growth in ‘soft adventure’ activities. There has also been related growth in safety standards imposed on providers by legislation and self-regulation. The early days of cowboy operators with dubious safety standards are long gone.”

A case in point, Sylvester says, is Vang Vieng in Laos, which became notorious after a series of fatal accidents involving river tubing, rope swings and waterslides, before local authorities clamped down on ad-hoc operators.

Collinson Group’s Lawson concurs, but says not all destinations live up to the standards set by countries like New Zealand. “There are two key influences on people’s growing approach to adrenaline/adventure travel,” Lawson said. “The first is that travel companies are increasingly moving away from typical beach/winter/city holidays and their inventory now often reflects new and exciting opportunities – itself a challenge when marketing to generations that have increasing disposable income and ability to travel. They have a greater reach of destinations and a growing market wanting to stretch their ambitions.

“Certain countries have understandably capitalised on the tourist attractions that exist in their region and, not surprisingly, that creates demand, even when there is an element of greater risk. Whilst some countries can show that their provision for such attractions has been supportive, such as New Zealand, others have maybe not got the same infrastructure in place when things go wrong.

“The other key driver is that we are in a social media world where showing people what you are doing, and where you have been, is a major part of the holiday. This has clearly driven people to push the boundaries. As an industry, all we can do is continue to monitor cause of loss, adjust our rating where we have to pay claims, but also ensure that our longstanding clauses of needless exposure to risk are translated at the point of sale into simple language – if you think it’s dangerous, and you still do it, don’t be surprised if you get hurt and need help. If you haven’t thought about travel insurance, don’t be surprised if that help costs.”

February 2020

Issue

In this issue of ITIJ, we have feature articles on Spring Break cover, changing the public perception of travel insurers, and volcano tourism; plus, a special report on the US air ambulance industry’s involvement in the current balance billing debate. We also interview Damian Lenihan of Aetna International about his role and approach to current industry challenges and opportunities; and we garner professional insights from International SOS on travel risk and Shift Technology on digitisation.

Elsewhere, insights into future travel trends are explored by Expedia, we assess the impact of the Australian bushfires, and we keep abreast of the latest regulations aimed at increasing safety on Mount Everest.

Robin Gauldie

Robin Gauldie is a freelance journalist and a former editor of a number of travel trade and specialist publications including Travel Trade Gazette Europe, ABTA Magazine, Ireland 2000 and Climate Change - Addressing the Challenge. He contributes to several newspapers and magazines including The Scotsman and Telegraph Travel and is the author of more than 30 travel guidebooks to destinations around the world. He lives in Edinburgh.

Robin has been writing for ITIJ and its Review publications on a freelance basis since 2008, covering a wide range of topics that span the global insurance and assistance sectors.